giphy

The fourth quarter sure didn't waste any time stirring the pot, with markets jittery over labor stats, port disputes, global tensions, and the looming the presidential showdown. However, some relief emerged as the week unfolded, aided by positive labor-market data and a tentative resolution to the port strike.

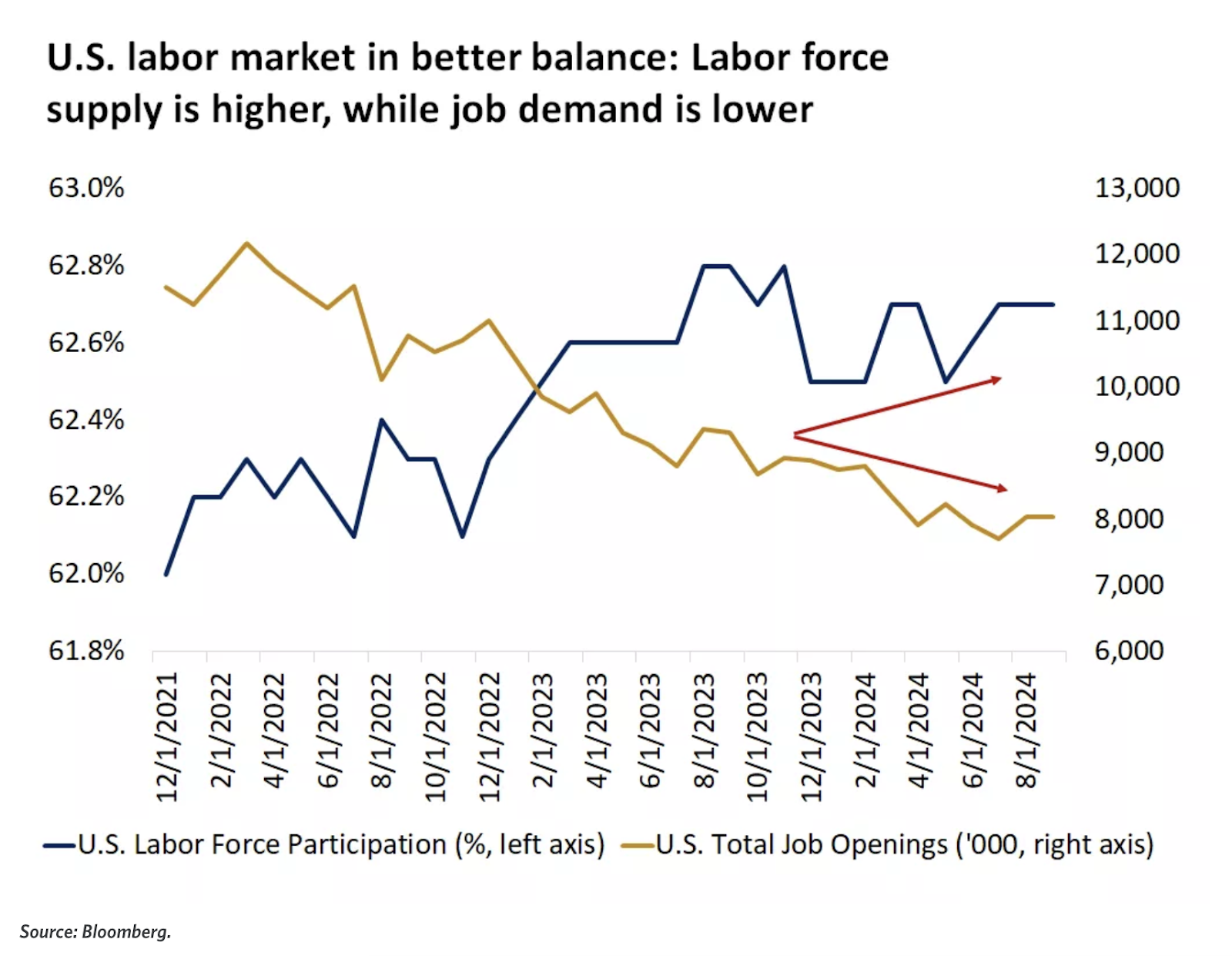

Labor Market Surprises — September's nonfarm-jobs report exceeded expectations, with 254K jobs added compared to the forecasted 150K. The unemployment rate dipped to 4.1%.

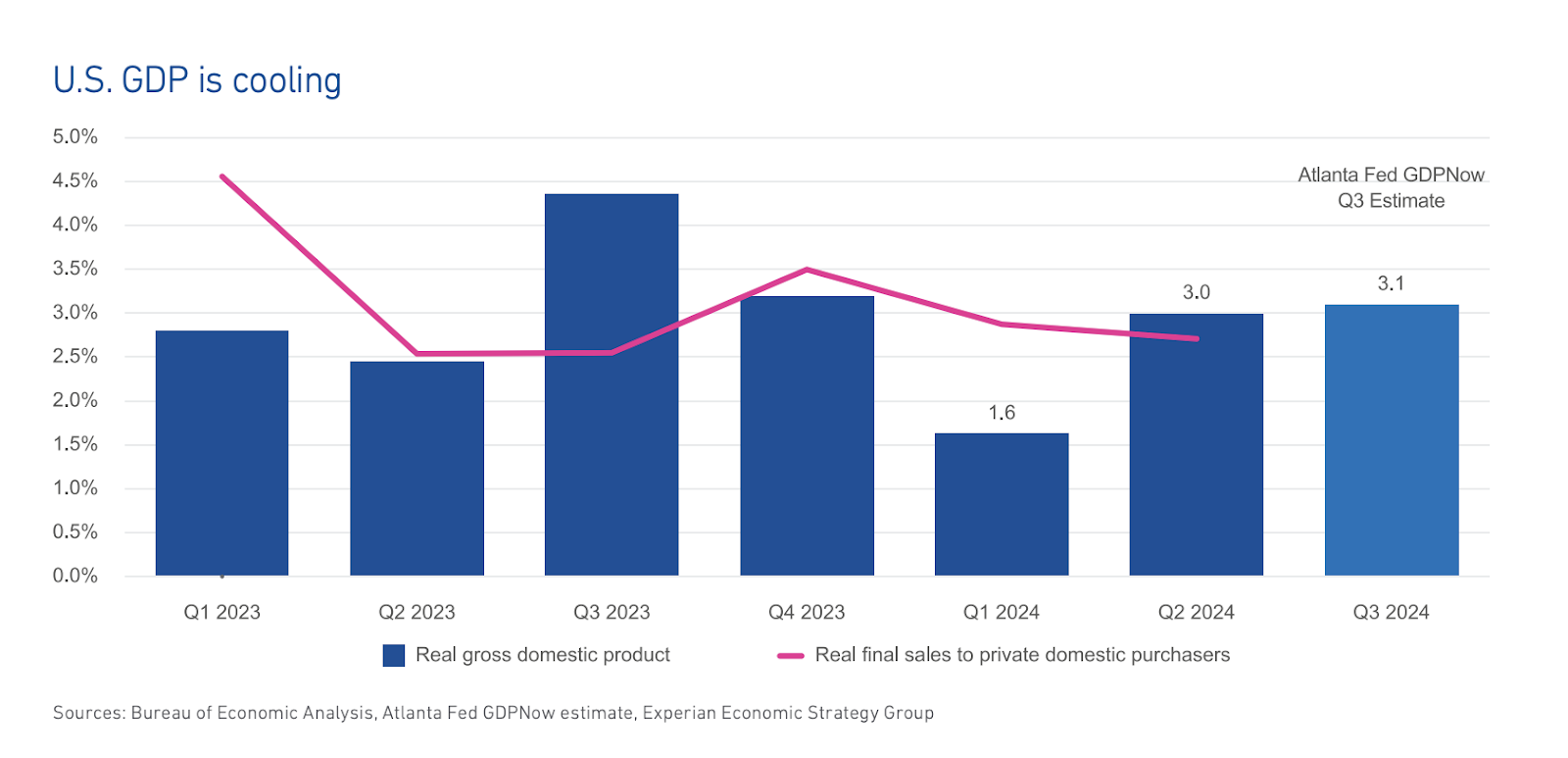

Solid Foundations — Despite lingering geopolitical uncertainties, the economy continues to grow. The Fed is expected to cut rates through 2025, and inflation is gradually moderating.

Edward Jones / FactSet

The strong labor report has also reshaped expectations for Federal Reserve rate cuts. Instead of a more aggressive 0.5% cut in November or December, markets are now pricing in a smaller 0.25% cut.

Rate Strategy — Economists expect the Fed to continue lowering rates gradually, aiming for a range of 3.0%-3.5% next year.

Slow and Steady — Wage growth remains steady at 4.0% year-over-year, keeping inflation concerns on the radar.

Data shows that U.S. consumers are continuing to tighten their belts and hold off on big buys and splurges. Even as inflation cools, it’s still got its claws in everyday costs, leaving less room for the fun stuff.

Big-Ticket Items Get the Cold Shoulder — By August, transactions over $1,000—think home renos or like, two airport sandwiches—dropped by 5.8%. Consumers aren’t keen on financing those pricier purchases when interest rates are still this high.

Retailers Feel the Pinch — Big box stores like Target have managed a 2% bump in same-store sales, but only after slashing prices on the basics. Home Depot echoed a similar story of cautious customers.

Experian / Bureau of Economic Analysis

Experian / Bureau of Economic Analysis / Atlanta Fed

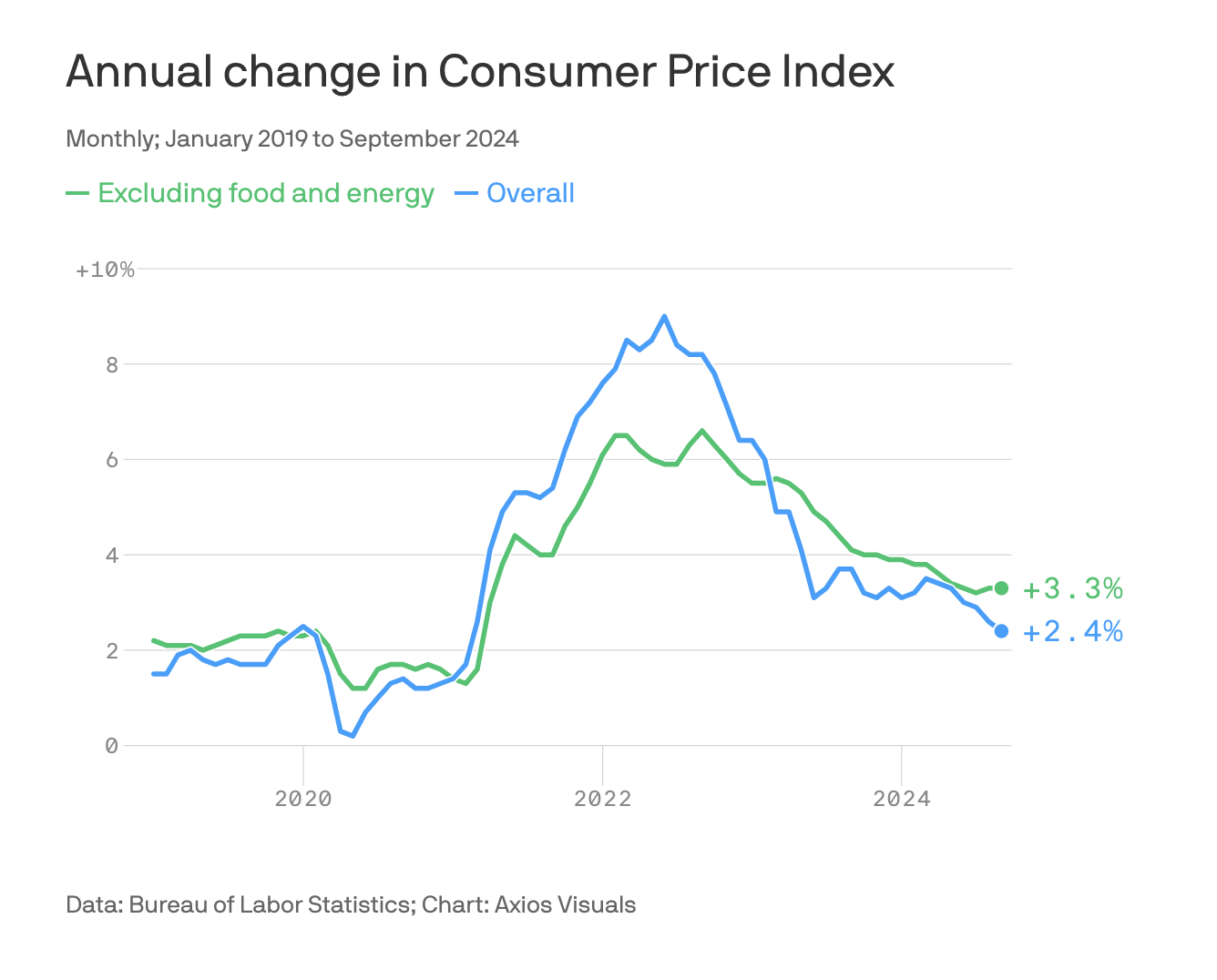

Thursday's CPI report shows progress, but the road to normalizing prices remains bumpy. While overall inflation is easing, sticky core costs keep the Fed on high alert.

Price Patterns — Consumer prices climbed 2.4% in the past year, marking the smallest increase since early 2021. But core inflation ticked up to 3.3%, showing that deeper price pressures are still in play.

Housing Trends — Rental costs showed signs of slowing, with shelter prices rising just 0.2% in September. It’s a positive shift, but the Fed remains cautious given the potential for temporary relief.

Rate Strategy — Despite a jumbo rate cut last month, Fed officials are signaling a measured approach going forward, with a likely quarter-point reduction in November amid lingering inflation concerns.

Axios / Bureau of Labor Statistics

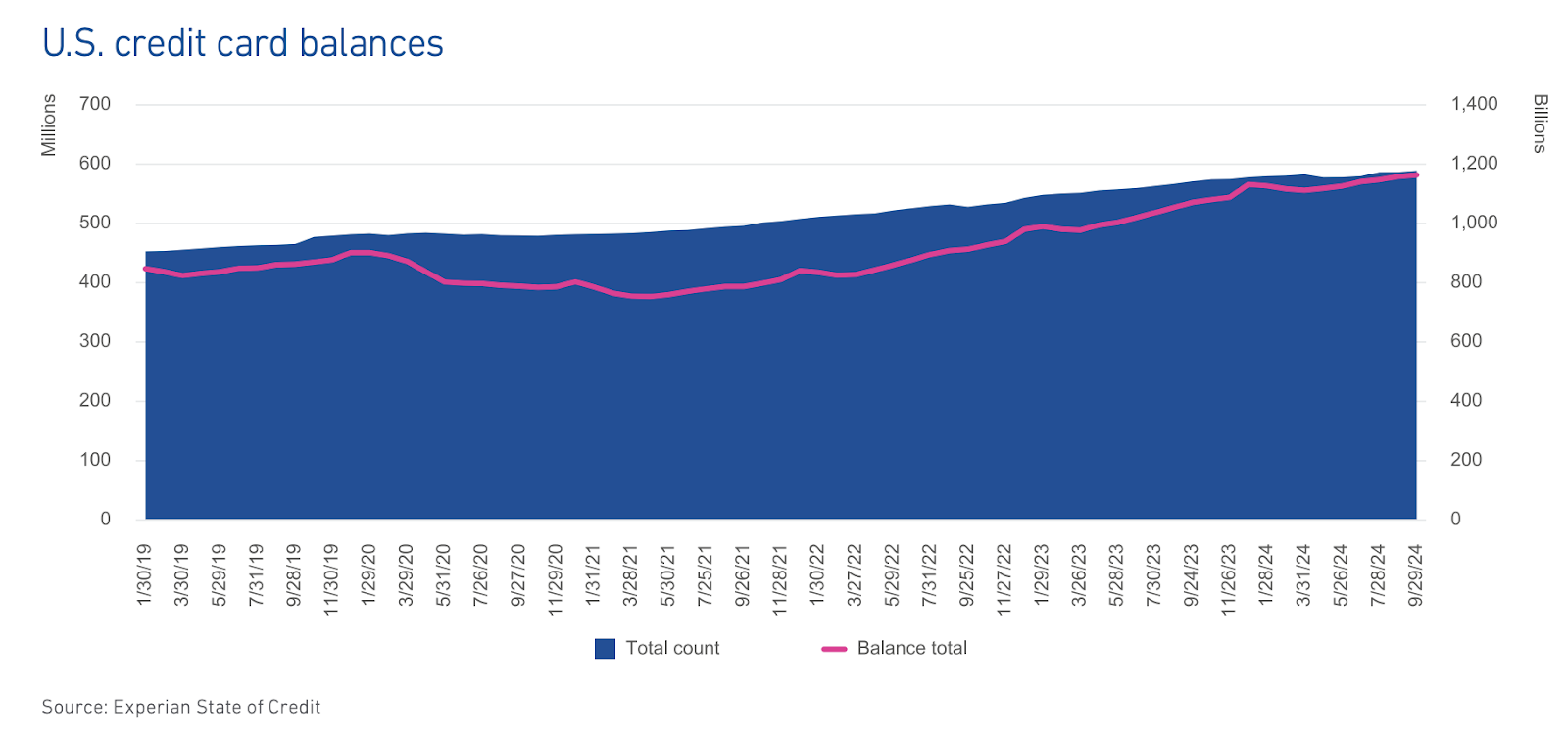

The consumer debt service ratio has climbed to 5.7%, exceeding pre-pandemic levels. Higher interest rates on loans like credit cards and auto loans mean households are dedicating more income to debt repayment, leaving less for holiday splurges.

Rising Debt Burdens — Credit card balances are up 9% year-over-year as more people lean on plastic to cover living expenses.

Borrowing Limits Tested — Although credit utilization hasn't hit pre-pandemic peaks, stricter lending standards and high rates limit how much more consumers can borrow heading into the holidays.

Experian

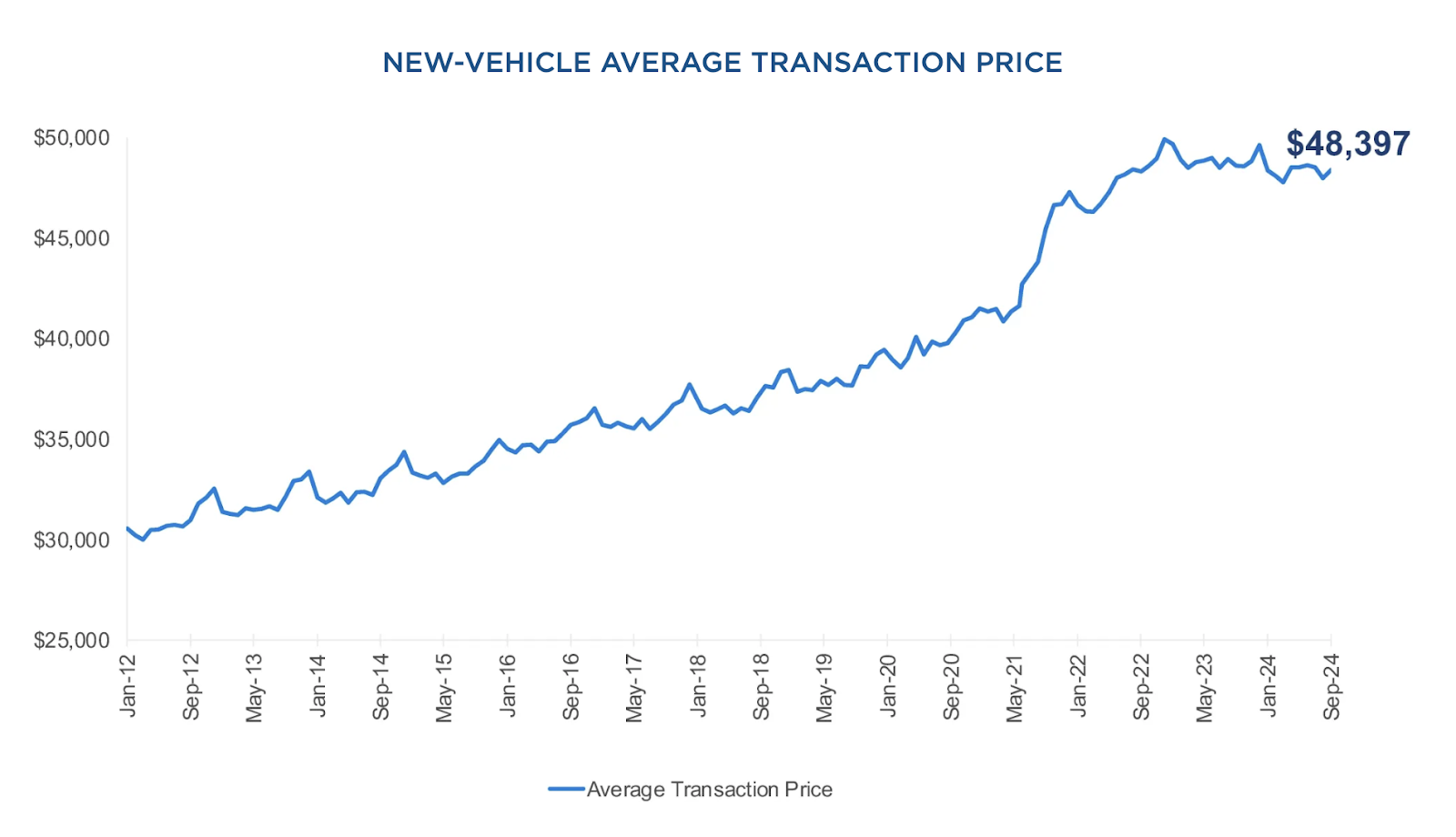

The average transaction price for new vehicles in September hit $48,397, down 0.4% from the same time last year. The downward pressure on prices continues, but the rise in incentives has kept the market moving.

Incentive Boost — Incentives reached 7.3% of the ATP in September, equaling around $3,522 per vehicle. That’s up from 7.2% in August and a big jump from 4.8% in September 2023.

Affordability Still a Challenge — Despite higher incentives, options under $20,000 are rare. The Mitsubishi Mirage remains the lone new vehicle in the U.S. priced below this threshold.

Cox Automotive

Last week, the used vehicle market faced increased uncertainty due to the duration of the dock workers’ strike and concerns over flood damage from Hurricane Helene. Higher floor prices at auctions led to more no-sales, even as the strike reached a tentative resolution. The full impact of the hurricanes that have recently hit the Southeast still remains unclear.

Car Segment Slips —The Car segment declined -0.22% overall, accelerating from a -0.10% drop the previous week. The 0-to-2-year-old Car segment fell -0.07%, while the 8-to-16-year-old segment dropped -0.34%. Compact Cars bucked the trend, rising +0.14%, with newer models (0-2 years) leading at +0.33%.

Truck Segment Takes a Hit — Trucks declined -0.32% overall, compared to -0.22% the prior week. The 0-to-2-year-old models dipped -0.21%, while older models (8-16 years) dropped -0.54%. Small pickups, which had seen seven weeks of gains, fell -0.49%, while sub-compact crossovers had the steepest drop at -0.75%.

Full-Size Pickups Face Pressure — Depreciation for full-size pickups increased, falling -0.20% from a -0.04% dip the previous week.

Blackbook

📬 For more data and stats like this delivered right to your inbox, subscribe to our daily email. 👇